First month of 2018, and it wasn’t the greatest month for my net worth compared to the last few months of 2017. We also have the market going haywire so far this month, so I don’t think I’ll be seeing any impressive gains at the end of this month either. The important part is that I am continuing the same pace of savings, and that should help to boost my portfolio at the time. I’m still making steady progress, and I’ll focus on my savings rate which I can control. The market will do what it wants, and over a longer timeline it should go up rather than down.

First month of 2018, and it wasn’t the greatest month for my net worth compared to the last few months of 2017. We also have the market going haywire so far this month, so I don’t think I’ll be seeing any impressive gains at the end of this month either. The important part is that I am continuing the same pace of savings, and that should help to boost my portfolio at the time. I’m still making steady progress, and I’ll focus on my savings rate which I can control. The market will do what it wants, and over a longer timeline it should go up rather than down.

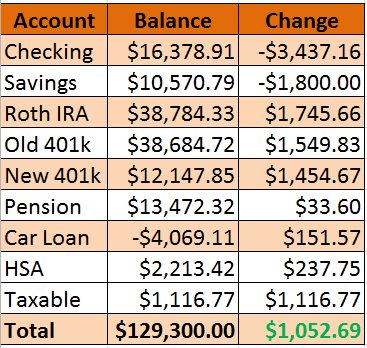

This is my net worth for January:

My checking and savings accounts took a hit, but that was to be expected as I had several bills that needed to paid in January. That is what caused the inflated total and huge spike in December, as I had a lot of extra cash sitting around in my accounts. The spending had already been accounted for, but the money had to be transferred to pay off the credit cards in full.

My checking and savings accounts took a hit, but that was to be expected as I had several bills that needed to paid in January. That is what caused the inflated total and huge spike in December, as I had a lot of extra cash sitting around in my accounts. The spending had already been accounted for, but the money had to be transferred to pay off the credit cards in full.

Every other account across the board managed to post strong gains, thanks to contributions and the market rallying throughout the month of January. I started a small taxable account for now, but don’t think I’ll be putting too much money into that account. I actually plan on increasing my 401k contribution by another percent before I start doing that. I’d rather take advantage of the tax savings instead of putting in the taxable just yet.

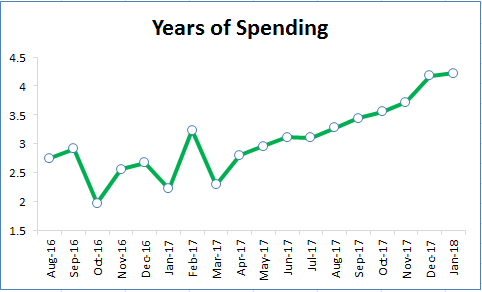

So let’s see how far my assets would actually take me at this point in time. I’m going to calculate that using my average spending over the last 12 months. I’ll then multiply that by 12 months to get the total spending for the year, and then divide my total net worth by that amount. That’s how long I’d be able to live off my savings at that point in time.

So let’s see how far my assets would actually take me at this point in time. I’m going to calculate that using my average spending over the last 12 months. I’ll then multiply that by 12 months to get the total spending for the year, and then divide my total net worth by that amount. That’s how long I’d be able to live off my savings at that point in time.

$2483 average spending last 12 Months * 12 Months = $29,779 spending in a year

$129,300 net worth / $30,673 spending per year = 4.22 years worth of spending

Relatively flat compared to last month, with spending decreasing slightly and my net worth increasing by around $1000. I was able to stay above that 4 year mark, and I’m hoping that I’ll be able to do that this month as well. The market has not been as kind in February so far, and I am planning on some large vacation spending in February and March.

I also thought it would be cool to see the opposite, how much would I be able to withdraw each month? I set the rate of return at 4% as a conservative guess, and the retirement time period would be for 30 years.

I also thought it would be cool to see the opposite, how much would I be able to withdraw each month? I set the rate of return at 4% as a conservative guess, and the retirement time period would be for 30 years.

I’d be able to withdraw $615 a month for 30 years which is 24.8% of my average monthly spending.

I set a stretch goal to be able to cover 35% of my spending by the end of the year, and I bumped it up by just under a percent during the first month. I’m still on pace to hit that goal, but I’m also expecting my average spending to go back up as I have yearly expenses and vacation expenses coming up on top of normal spending. If my net worth can continue to rise, I think that will help in balancing things out. But it may just remain steady if the market is flat or down.

Leave a Reply