We are now 17 days into the new year, yet I’m still typing/writing out 2017 whenever doing anything. Hopefully I’ll get over that by the end of the month! It’s time to bring you the second edition of my early retirement tracker, where I take a look behind exactly how much I need to save, and for how much longer. I started tracking this back in October, but just published the first post in December to establish a bit of a trend before I shared it with the world. I think that watching the years count down are a huge motivation for me, probably even more so than watching my portfolio grow. And that’s not to say I am wishing away this time, I intend to fully enjoy my time both while working and when financially independent.

We are now 17 days into the new year, yet I’m still typing/writing out 2017 whenever doing anything. Hopefully I’ll get over that by the end of the month! It’s time to bring you the second edition of my early retirement tracker, where I take a look behind exactly how much I need to save, and for how much longer. I started tracking this back in October, but just published the first post in December to establish a bit of a trend before I shared it with the world. I think that watching the years count down are a huge motivation for me, probably even more so than watching my portfolio grow. And that’s not to say I am wishing away this time, I intend to fully enjoy my time both while working and when financially independent.

A reminder of the three ways I will tracking my progress:

- The first way will actually be with a simple excel calculator that I made. I’ll plug in my current monthly expenses, savings rate, and net worth. And the calculator will say just how long I have until retirement. Maybe it will say that I can retire tomorrow?

- The second way I’ll be calculating this is through an equation and the help of Wolfram Alpha.

- The third and final way I’ll be calculating my early retirement date is with the help of Mad Fientist Laboratory. I’ll input expenses, savings, and net worth and let his calculations do the rest of the work.

Retirement estimation based on 4% market growth:

Retirement estimation based on 7% market growth:

Retirement estimation based on 7% market growth:

I’m making excellent progress based on these estimations! Down to 16.4 years at 4% growth, and only 12.6 years at 7% growth. The cool thing is that if you take 1/12 of the year for a month, you end up with .08 of the year. So if you saw the numbers going down by .1, that would essentially just be the passing of time as I move closer to the target. But so far, every time that I’ve ran the calculation the number has actually decreased by more than that!

I’m making excellent progress based on these estimations! Down to 16.4 years at 4% growth, and only 12.6 years at 7% growth. The cool thing is that if you take 1/12 of the year for a month, you end up with .08 of the year. So if you saw the numbers going down by .1, that would essentially just be the passing of time as I move closer to the target. But so far, every time that I’ve ran the calculation the number has actually decreased by more than that!

I am sure that the market is a huge help, but I’m trying to keep my savings rate as high as possible in order to keep that number moving in the right direction. I’m thinking that by the end of 2017 I’ll have a much better estimation as the portfolio grows and the contributions matter less and less.

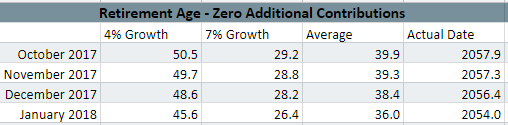

Retirement estimation if I never save another dollar:

I believe that last time I had referred to this as my coast point, if I spend all my income and don’t save a single penny. I’d still be on track to retire in 36 years, which basically puts me on track for a “normal” retirement age (in between 62-67). It’s great to see that my savings so far has secured my future, even if for some reason I wouldn’t actually be able to continue to save at my current rate. This is definitely the reason why everyone says to “save early and save often”

I believe that last time I had referred to this as my coast point, if I spend all my income and don’t save a single penny. I’d still be on track to retire in 36 years, which basically puts me on track for a “normal” retirement age (in between 62-67). It’s great to see that my savings so far has secured my future, even if for some reason I wouldn’t actually be able to continue to save at my current rate. This is definitely the reason why everyone says to “save early and save often”

Leave a Reply