I’m continuing the trend to track my progress into early retirement, even if I am a little late with this post this month! The numbers were all calculated ahead of time, I just had to find time to write the actual post. Net worth growth was slow in January so I felt like that would slow progress when it came to early retirement, but it seems like I’m still moving in the correct direction even with the mostly flat progress. Spending has been trending down lately, but I expect that to rise like I had mentioned in a previous post. I do love putting a date to everything, as that gives me a tangible goal to work towards – even if it just an estimation at this point.

I’m continuing the trend to track my progress into early retirement, even if I am a little late with this post this month! The numbers were all calculated ahead of time, I just had to find time to write the actual post. Net worth growth was slow in January so I felt like that would slow progress when it came to early retirement, but it seems like I’m still moving in the correct direction even with the mostly flat progress. Spending has been trending down lately, but I expect that to rise like I had mentioned in a previous post. I do love putting a date to everything, as that gives me a tangible goal to work towards – even if it just an estimation at this point.

A reminder of the three ways I will tracking my progress:

- The first way will actually be with a simple excel calculator that I made. I’ll plug in my current monthly expenses, savings rate, and net worth. And the calculator will say just how long I have until retirement. Maybe it will say that I can retire tomorrow?

- The second way I’ll be calculating this is through an equation and the help of Wolfram Alpha.

- The third and final way I’ll be calculating my early retirement date is with the help of Mad Fientist Laboratory. I’ll input expenses, savings, and net worth and let his calculations do the rest of the work.

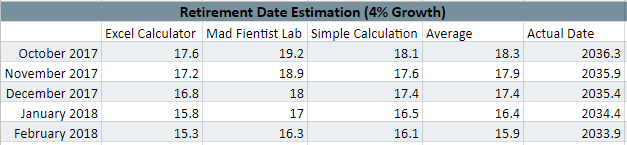

Retirement estimation based on 4% market growth:

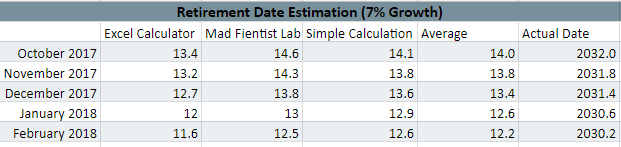

Retirement estimation based on 7% market growth:

Retirement estimation based on 7% market growth:

I’ve managed to squeak under 16 years even with only 4% growth estimates, which is really impressive to me! Also quickly closing in on 12 years until retirement with 7% growth, which is where I’m honestly expecting the numbers to settle as we progress through the year. Based on my spending targets and savings rate, I think that is more of an accurate prediction of when I’ll actually be able to retire.

I’ve managed to squeak under 16 years even with only 4% growth estimates, which is really impressive to me! Also quickly closing in on 12 years until retirement with 7% growth, which is where I’m honestly expecting the numbers to settle as we progress through the year. Based on my spending targets and savings rate, I think that is more of an accurate prediction of when I’ll actually be able to retire.

I’m still dropping the amount of years faster that time is advancing, which is a great sign. I’m very curious about March numbers because of market hitting a lull recently. I feel like my portfolio is slowly approaching a tipping point where the savings rate will be less important and the market’s movement will have a greater effect on my money.

Retirement estimation if I never save another dollar:

This is my coast point, where I wouldn’t have to save any additional money and would still have enough to retire. The average is coming out to 35.2 years now, which still puts me in that 62-67 age range for a “normal” retirement at this point. The important thing here is that this number continues to drop and as my portfolio increases we should see the gap between this and my early retirement age get closer and closer. I’m hoping that by the end of 2018 this number will be under 30 years.

This is my coast point, where I wouldn’t have to save any additional money and would still have enough to retire. The average is coming out to 35.2 years now, which still puts me in that 62-67 age range for a “normal” retirement at this point. The important thing here is that this number continues to drop and as my portfolio increases we should see the gap between this and my early retirement age get closer and closer. I’m hoping that by the end of 2018 this number will be under 30 years.

Hey, three ways tracking sounds good. The whole article really helpful and informative for me to track my own. Thanks for sharing