Time for my monthly update on my net worth. I’m hoping for warmer weather to start to arrive after what feels like a long winter, even if it may have not been bitter cold. I’m ready to get outside and start doing things! I’m sure everyone in the personal finance blogosphere has been paying attention closely to this “trade war” and the resulting effects that it is having on the market. I’m just hoping that these tariffs don’t have too many unforeseen consequences that send us into a recession, and hoping that reasonable heads can prevail.

Time for my monthly update on my net worth. I’m hoping for warmer weather to start to arrive after what feels like a long winter, even if it may have not been bitter cold. I’m ready to get outside and start doing things! I’m sure everyone in the personal finance blogosphere has been paying attention closely to this “trade war” and the resulting effects that it is having on the market. I’m just hoping that these tariffs don’t have too many unforeseen consequences that send us into a recession, and hoping that reasonable heads can prevail.

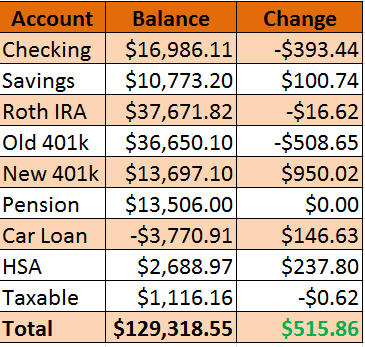

Here is my net worth after March:

I had a slight gain this month, basically bringing my net worth back up to the same level that it was in January. The market took a dip at the end of March which erased any gains that were had at the beginning of the month. We’re now trading at the levels seen in December, so the gains are only from my contributions at this point.

I had a slight gain this month, basically bringing my net worth back up to the same level that it was in January. The market took a dip at the end of March which erased any gains that were had at the beginning of the month. We’re now trading at the levels seen in December, so the gains are only from my contributions at this point.

Both my Old 401k and Roth IRA both saw losses this month, though they weren’t as steep as the past month. We will see what the rest of April brings, but so far the market has been flat. My guess is that with contributions I will be able to slide past the 130,000 mark this coming month.

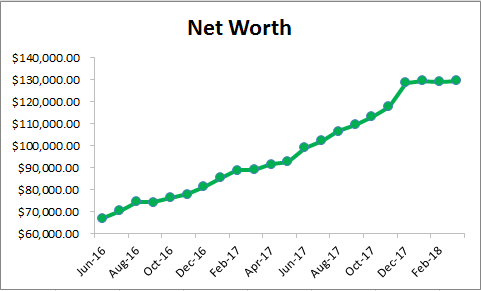

You can see that plateau starting to form after all the gains over the past year. Hopefully I can start to increase that climb once again!

You can see that plateau starting to form after all the gains over the past year. Hopefully I can start to increase that climb once again!

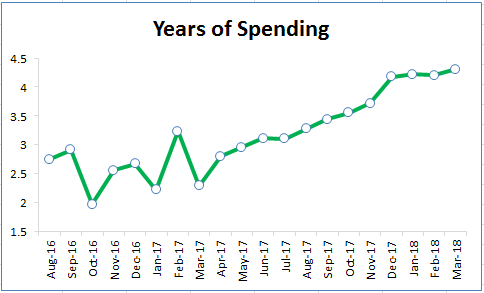

So let’s see how far my assets would actually take me at this point in time. I’m going to calculate that using my average spending over the last 12 months. I’ll then multiply that by 12 months to get the total spending for the year, and then divide my total net worth by that amount. That’s how long I’d be able to live off my savings at that point in time.

$2502 average spending last 12 Months * 12 Months = $30,024 spending in a year

$129,318 net worth / $30,024 spending per year = 4.31 years worth of spending

I’m barely at my highest mark on this chart, thanks to a slight bump up in net worth and a slight decrease in spending. I’ll essentially call this one flat as well though.

I also thought it would be cool to see the opposite, how much would I be able to withdraw each month? I set the rate of return at 4% as a conservative guess, and the retirement time period would be for 30 years.

I also thought it would be cool to see the opposite, how much would I be able to withdraw each month? I set the rate of return at 4% as a conservative guess, and the retirement time period would be for 30 years.

I’d be able to withdraw $615 a month for 30 years which is 24.6% of my average monthly spending.

I’m back up to the same rate that I was at in January, with 35% of spending looking a long way off. We do still have plenty of time in 2018 though. I’m hoping that even if the market remains flat, I’ll personally be able to get to 30% from just contributions.

Just want to say what a great blog you got here! I have been around for quite a lot of time, but finally decided to show my appreciation of your work! You are really doing well for your readers. Each and every post you shared here is worth reading. This blog is definitely entertaining and factual. I have picked up a bunch of interesting advices out of this blog. I would love to come back again and again. Thanks a bunch!